+91-080-6821-6821

9:30 AM - 6:30 PM

(Mon-Sat)

(Mon-Sat)

NBFC-P2P

Registered with RBI

CoR No. N - 13.02258

NBFC-P2P

Registered with RBI

CoR No. N - 13.02258In reference to the Reserve Bank of India (RBI) circular, Master Direction DNBR (PD) 090/03.10.124/2017-2018, dated October 4th, 2017, wherein RBI has laid down guidelines on Fair Practices Code for Non-Banking Financial Company- Peer to Peer Lending Platforms, OHMY Technologies Pvt. Ltd., (OMTPL, "OMLP2P.COM"), a P2P lending platform, has formulated its FPC which covers directions, policies, processes, risk associated to prospective lenders and borrowers while conducting transactions on our platform. It also provides information around how platform is expected to deal with any issues arising pertinent to FPC on a day to day basis. This policy applies to all customer including those with any complaints as posted social or any other media and we encourage all customers to reach out to the below platforms as required.

OMTPL provides a platform for connecting the Borrowers and the Lenders to facilitate borrowing and lending on or through this Website and such services that are incidental, ancillary or connected therewith. OMTPL or this Website does not take responsibility or liability to match the Borrower with the Lender or vice versa and/or to ensure the giving or procurement of a Loan and/or recovery of a Loan. OMTPL does not make any promise and/or representation that your loan requirement will be listed and/or satisfied on this Website and/or that a Loan will be provided to you. OMTPL does not take any responsibility or liability regarding the negligent acts or omissions of the Borrower or the Lender. OMTYPL want to further re-stress and explicit consent from the lenders that-

OMTPL is engaged in the business of running an online peer-to-peer lending platform that connects potential borrowers and lenders and through its Website facilitates the borrowers to raise and the lenders to finance unsecured / secured personal and business loans. The Borrower has on the Website applied for a loan and the Lenders have agreed to finance an amount as mentioned herein relying on the covenants of the Borrower and the representations and warranties contained herein.

In the event of default (as mentioned in the loan agreement), the Lenders either individually or collectively, and/or OMTPL (acting on behalf of the Lenders, at its sole discretion and subject to Applicable Law) and/or any Person acting on their behalf may, at their discretion, by a notice in writing to the Borrower and without prejudice to the rights and remedies available to Lenders under this Loan Agreement and/or any other Transaction Document or otherwise call upon the Borrower to pay all the Borrower’s dues in respect of the Loan. In the matter of recovery of outstanding dues of its Borrower, OMTPL (if agreed to get engaged in recovery process on lenders behalf) does not resort to undue harassment viz. persistently bothering the borrowers at odd hours, use of coercion for recovery of loans /dues, etc. Training will be imparted to ensure that staff is adequately trained to deal with customers in an appropriate manner.

OMTPL collects and retains all data pertaining to customers either as a User and/or Registered User and/or a Borrower and/or a Lender, as mentioned in section 4.3 of the privacy policy. OMTPL is committed to securing any Data you entrust to us and follows generally accepted industry standards in its endeavor to protect the same, during transmission, reception, etc. We use Secure Sockets Layer (SSL) technology to encrypt any Data you provide while using this Website or while availing any Service offered thereunder.

We have constituted a Fair Practice Code Compliance Committee to review the implementation at periodic intervals and furnish feedback on the same to the Board of Directors at their review at half-yearly intervals. We shall incorporate verification and checks for compliance of all the practices through the specific designed officials in the hierarchy and through effective internal audit/ periodical inspections.

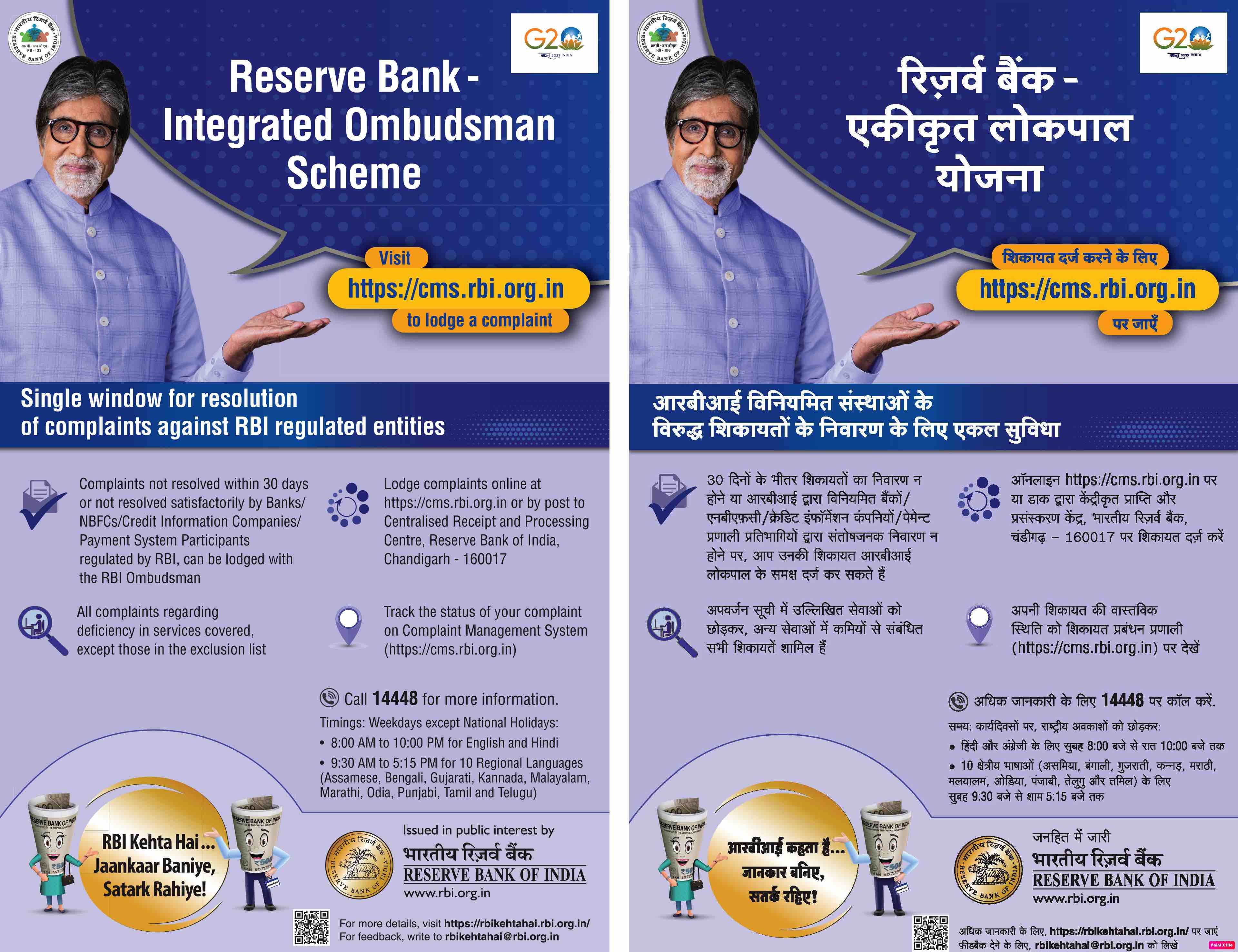

If the complaint/dispute is not redressed within a period of one month, the participant may appeals to the customer education and protection department of the bank.

© 2020, omlp2p.com - All Rights Reserved

NBFC-P2P

Registered with RBI

{kind=link}

{kind=link}